Among the various Australian mortgage loan features on offer, “Line of Credit Vs Offset” seems to be the most debated over others.

Many property investors are usually confused about the difference between a line of loan and an offset account.

There are several other loan features available, and lenders are still coming up with new features to offer borrowers more options.

Understanding how these two loan features function will help determine the best fit for you. Here, we will consider a line of credit vs offset account and when to use either of them.

Related Articles

- 10 Tips on how to buy an investment property

- Beginner Investor guide: Building your property portfolio

- How does equity work when buying a second home?

What’s a Line Of Credit

A line of credit is otherwise known as a home equity loan or home equity line of credit (HELOC). This feature lets you borrow money with your existing equity.

A line of credit poses as a flexible transactional loan giving you the freedom to access your funds anytime you need them. Hence, you can use it at your discretion.

For instance, you could use the funds to handle your home renovation, personal purchases like home items, or property investment. If you’re considering an investment loan, understanding how a line of credit can support your investment goals is crucial.

What are the disadvantages of a line of credit?

The downside with a line of credit is unless you are disciplined, you could end up finding yourself accessing the available fund through the LOC for non-investments. For example, items without a return.

Due to that, your debt won’t be reduced effectively, and things could easily get out of hand.

You should consider LOCs for active accounts like investment portfolios where you regularly trade to reconcile the balance on a daily, weekly, or monthly basis.

When a line of credit is secured by property, the credit limit would be much higher than that of a credit card. Also, the interest rate is usually lower.

Unlike traditional loans, you only pay interest on the amount you draw from a line of credit.

Like a credit card, a line of credit has a fixed credit limit. Funds are easily accessible at any time via debit card, cheque, or internet banking.

Managing a line of credit alongside your home loan can provide additional financial flexibility.

This implies that repayment would not be necessary until the facility is fully drawn. In other words, the owed balance is equal to the fixed credit limit.

A line of credit is considered a helpful tool for investment, given that it assists with your investment property cash flows.

Another downside to note about a line of credit is that you may sometimes pay an interest rate on the facility due to the transactional nature of the facility.

Also, the idea of the lender retaining capital aside for the facility limit, regardless of whether you use the available funds in full or not.

The interest rate difference between a home loan and a line of credit can be about two per cent or more.

Like a credit card, a line of credit has a fixed credit limit. Funds are easily accessible at any time via debit card, cheque, or internet banking.

Interest can be settled only on drawn funds. This is made possible with some available line of credit products to capitalize the interest.

This implies that repayment would not be necessary until the facility is fully drawn. In other words, the owed balance is equal to the fixed credit limit.

A line of credit is considered a helpful tool for investment, given that it assists with your investment property cash flows.

Another downside to note about a line of credit is that you may sometimes pay an interest rate on the facility due to the transactional nature of the facility.

Also, the idea of the lender retaining capital aside for the facility limit, regardless of whether you use the available funds in full or not.

The interest rate difference between a home loan and a line of credit can be about two per cent or more.

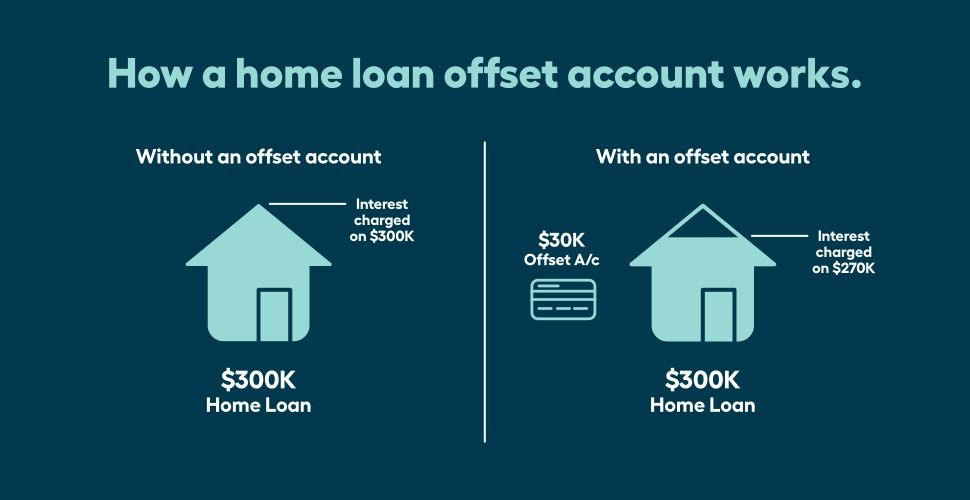

What are offset accounts?

An offset account is simply an account that you can link to your mortgage or investment loan.

The credit balance of the transaction account is offset daily against your loan balance, drastically reducing the payable interest on the loan.

Using an offset account can significantly reduce your home loan interest over time.

These funds are always accessible, and yet, while they cool off in the bank, they work for you as they help reduce the accruing interest on the mortgage loan.

In other words, it is an effective tool to reduce loan interest and separate funds for tax payments.

Instead of earning interest through savings, the savings balance is deducted from the loan balance, which reduces the interest on the loan.

One benefit of an offset account is that it can help manage tax implications, as the interest saved is not considered taxable income.

Another advantage here is that the ATO does not take this as an earning interest income. Hence the good stuff is gotten without more tax expenses.

Furthermore, an offset account can help reduce the loan term and give you the freedom to keep your funds at call and used to handle any purpose.

Two Different Types of Offset Accounts

- 100 percent offset

All available funds are offset against the loan balance, working to reduce interest rate charges in this account.

- Partial offset:

A portion of the available funds is offset against the loan balance in this account.

These are just some key points to clear the air on the line of credit vs offset. Several loans will have a line of credit and offset available for borrowers.

However, they might not just suit you for one reason or another. If you are choosing loans and you find out that some loans include features different from each other, then you might want to stop and ask these questions:

- Are there fees for the extra features?

- Will the interest rate increase due to these additional features?

- What should I look for most in a loan?

- Am I likely to use this loan?

- Will I be able to save any money just by using these features?

Factors to consider before choosing an offset account vs line of credit

Factors to consider before choosing an offset account vs line of credit

While you consider a line of credit vs offset to know which one is worthwhile, you should consider a few factors.

Linking your offset account to your investment property loan can provide significant interest savings.

- Determine how much the upfront charges or present increased rate will cost throughout the loan duration compared to how much either of these features will save you. If you do not imagine yourself using the feature, it may not be perfect for you.

- Monitor the comparison rate to determine how the loan feature works out. Is the outcome good enough to cover poor performance when matched with other available loans in the market?

- Be aware of the tax implications when choosing between an offset account and a line of credit, especially for investment properties.

- Consider consulting your mortgage broker first to know your options before making choices.

Do not forget to thoroughly go through all the offered benefits to run your checks. Reduced ongoing expenses and waived application charges will likely outweigh any interest rate reduction on other loans.

Consulting a mortgage broker can help you understand which loan features will best suit your financial situation.

However, the money and total expense should not be the only consideration. If you want to have more flexibility and convenience, you may go for other certain features.

Usually, the red flags include one-off vouchers for certain services or active advisory on your loan.

For example, financial planning gift cards can be included coupled with property reports and using software to help you out.

Even if these may be attracting bonuses, it does not necessarily mean that the mortgage loan is fit for you.

Some fees are waived and offer cashback bonuses, but you might want to sum things up in the long term to know if the total cash back and savings would be equal.

In most cases, lenders offer incentives with the same rates, and at this point, it is all left to you to know how to go about the offset vs line of credit and figure out which works best for you.

FAQ Section on “Line of Credit vs Offset”

What should I consider when deciding to use an offset account?

An offset account can be highly effective in managing the interest on your home loan. When interest rates are low, it’s advantageous to explore options to accelerate your home loan repayment, such as increasing the frequency and amount of your repayments.

What is an offset on a line of credit?

An offset loan is a financing arrangement, typically used for mortgages, where the borrower also maintains a savings account with the lending institution.

The interest on the loan is calculated based on the net balance, which is the loan amount minus the savings in the account, thus potentially reducing the interest payable.

What is the main advantage of a line of credit over an installment loan?

A line of credit offers ongoing access to funds, allowing you to borrow, repay, and re-borrow as needed. Interest is charged only on the amount utilized, providing flexibility compared to an installment loan where the full loan amount plus interest is repaid over a set period.

What is the key difference between a loan and a line of credit?

A loan provides a fixed lump sum of money that is repaid over a designated period. In contrast, a line of credit allows you to borrow up to a specified limit, repay the borrowed amount, and borrow again, offering continuous access to funds.

Like what you’re reading?

Keep yourself updated with useful tips like these by downloading our app for the full Soho experience. Not only are we finding you your dream home, but we’re also helping yousave for it and decorate it! So don’t forget to swipe on your property matches so we can get you there faster.